The Telstra Corporation Ltd (ASX: TLS) share price has bounded higher over the past year, which is great unless… you’re me.

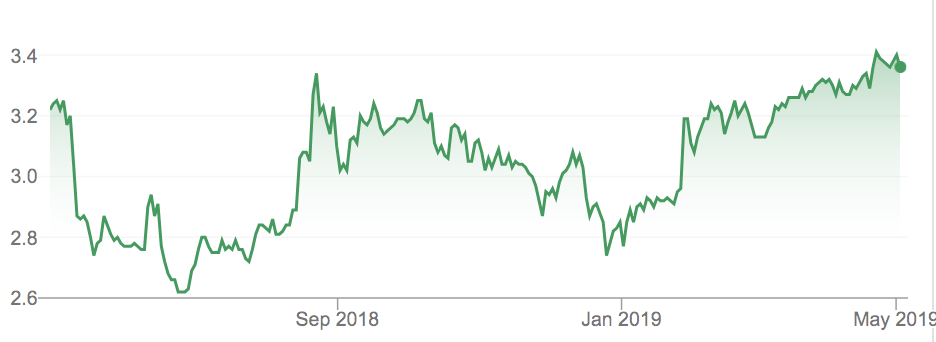

Telstra Share Price 2018/2019

About Telstra

Despite going head-to-head with rivals like SingTel Optus, Hutchison’s (ASX: HTA) Vodafone, Vocus Group Ltd’s (ASX: VOC) Dodo and TPG Telecom Ltd (ASX: TPM), Telstra is still our country’s dominant telecommunications business.

As of 2019, Telstra provides more than 17 million retail mobile services, around 5 million retail fixed voice services (e.g. home phones) and 3.6 million broadband services. Telstra also has operations in eHealth, network applications and subsea cabling.

Telstra is also our country’s oldest telecommunications business, having built the first telegraph line in 1854. In 1997 (until 2006), the Government sold Telstra to Australian investors by listing the shares on the ASX. The second batch of Government share sales, called “T2”, was conducted in 1999 at $7.40 per share.

Was I Dead Wrong About Telstra?

About a year ago I predicted Telstra’s share price to stay lower for longer. I was wrong about that.

I thought the NBN would swoop in and squeeze Telstra’s profit margins on broadband packages, which have been a key source of cashflow for the company.

I also predicted Telstra to cut its dividend in 2019 simply because it would be required to be financially prudent. I was right about that.

However, I wasn’t right about how the market would take the decision to cut the dividend. I expected ‘the market’ to react negatively to the news of a lower dividend because, well, everyone loves a fully franked dividend, right?

With the share price rising from a low of $2.60 ish in June 2018 to over $3.30 today, clearly, analysts and investors were pleased with the company’s decision to build its cash war chest to invest in growth areas and infrastructure for things like 5G mobile, innovative smarthome technology and network communications.

What’s more, with every passing day and another delayed NBN install, investors seem to be growing increasingly confident that 5G networks like Telstra’s — and Optus’ $70 unlimited packages — will provide the future of Australia’s internet connectivity. So rather than hook an ethernet cable to a router, people will simply use the nearest 5G tower to stream Netflix, even if the tower is 1km from their home.

Buy, Hold or Sell

Okay, yes, I didn’t expect Telstra’s share price to rise so quickly year-over-year, so take my opinion with a pinch of salt if you will.

However, despite its short-term share price performance, I continue to believe Telstra shares will struggle to beat the market over the next three-to-five years. It may beat the market if it maintains its dividend but if it doesn’t I struggle to see where growth will come from. More cost-outs perhaps?

Indeed, I do not believe 5G mobile will be the profit elixir that some investors think it may be. The Telstra 5G network’s range and reliability might afford it some pricing power, sure. But with Optus already offering unlimited 5G packages in select major cities, having a 5G network ready to roll in 2020 could be table stakes for Australia’s largest telcos.

I prefer to buy shares in companies with enduring competitive advantages or ‘moats’, similar to those three ASX companies found in the free report below.

[ls_content_block id=”14945″ para=”paragraphs”]

Disclosure: At the time of publishing Owen Raszkiewicz does not have a financial interest in any of the companies mentioned.