Damien Klassen from Nucleus Wealth explains why some Superannuation members could be about to be served a lemon.

Most superannuation funds, and especially industry funds have significant balances in unlisted assets. Many are telling you that these assets haven’t lost money, or are only down a little despite sharemarkets being down close to 30%. This gives rise to perverse incentives for superannuants:

- If you leave one of these funds now, you will get paid at the high prices for unlisted assets

- Anyone left behind bears the brunt of the losses

Rough numbers? I suspect right now that the median superannuation fund will pay you about 7% to leave.

Disclosure: Some of this is probably sour grapes! I run a superannuation fund that only buys liquid assets in separately managed accounts. So, an investor’s return is their return. We can’t rely on tax mingling, unlisted asset revaluations or other accounting tricks that master trusts use.

Featured podcast: Damien Klassen, Nucleus Wealth

The podcast episode above comes from The Australian Investors Podcast, Australia’s pre-eminent podcast for serious investors. To listen to the latest podcast with Damien and subscribe to the series, click here.

Background

Chant West gave us a quick preview of superannuation fund returns for March:

From Chant West:

“Growth funds, which is where most Australians have their superannuation invested, hold diversified portfolios that are spread across a wide range of growth and defensive asset sectors. This diversification works to cushion the blow during periods of share market weakness. So while Australian and international shares are down at least 27% since the end of January, the median growth fund’s loss has been limited to about 13%.”

Calculation

Some quick maths.

Chant West’s definition of a growth fund is one that has 60-80% of its assets in growth equities.

Let’s call it 70% exposure to shares, 5% cash and 25% to a composite bond fund.

If shares are down “at least” 27%, cash is unchanged, and a composite bond fund is down about 5%, then the implied return is a loss of -20%.

Chant West says the loss is only 13%.

There is 7% missing.

And that assumes that the 25% is in composite bonds, more likely it is higher risk unlisted assets.

So where is the missing money?

Now, individual funds will have different performance obviously. Our own growth fund is down less than 1% over the same time frame, but we took dramatic and aggressive measures at the end of January that I know others did not.

The superannuation market is $3 trillion. It is the market. If, somehow, almost every superannuation fund worked out the same thing we did and sold equities at the end of January, the market would have fallen in January. They didn’t.

The answer is superannuation funds have unlisted assets that they are not writing down. They are pretending that the prices are mostly unchanged from January.

What about the recently announced writedowns?

A few industry funds have written down assets. For example, AustralianSuper has revalued its unlisted infrastructure and property holdings downwards by 7.5%.

Um, have they looked at the rest of the market? The listed property sector is off more than 40%. Airports? Down 30%+. Private Equity? Ha! You are telling me that illiquid shares are worth a few per cent less while listed shares are down 25%+ and illiquid bonds aren’t even trading?

The writedowns help, but are nowhere near the level the assets would sell for today.

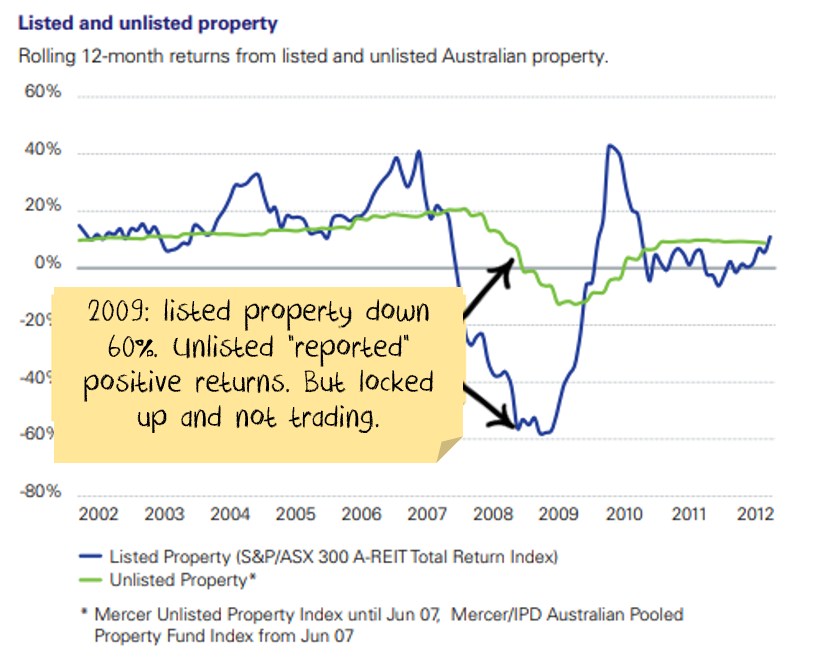

Financial Crisis Comparison

A great example is unlisted property funds during the financial crisis. Unlisted property funds invest in effectively the same assets as listed property funds, the underlying properties are worth the same, the performance differs because of how it is reported:

The perverse superannuation incentive

The problem is that if you own a fund that reports like this, you can be diluted if other investors leave. And any contributions you make now are at inflated prices. To illustrate with an extreme example, let’s say:

- You and I are the only investors in a super fund with $100 each invested

- The fund owns 50% an unlisted asset and 50% cash. So, the total value of the fund is $200 made up of $100 in the asset and $100 in cash.

- The asset falls 60% ($60) in price, so our fund is now only worth $140 ($70 each, we both should take a 30% loss), but the fund doesn’t revalue the asset and so reports the fund still being worth $200.

- I decide to redeem my holding in the fund.

- The unlisted asset can’t be easily sold, and so the fund pays me $100 cash being half of the $200 that the fund is still being officially valued at. I’ve broken even!

- This leaves you with $40 of unlisted assets – a 60% loss which is double the loss that you should have taken.

Adding insult to injury

The other problem with a typical superannuation fund (but not some of the newer ones that use a separately managed account structure) is your tax is mixed with other investors. Rodney Lay from IIR recently highlighted the issue:

…unit trust investors face another risk – being subject to the taxation implications of the trading activities of other investors. Net redemption requests may require the manager to sell underlying portfolio holdings which, in turn, may crystallise a capital gain… …During the GFC some investors had both (substantial) negative returns plus a tax bill on the fund’s crystallised gains. Good times!!!

Net effect

So, if you are a loyal soldier sticking with a superannuation fund that continues valuing unlisted assets at last year’s prices then:

- You are going to absorb the losses of anyone that leaves

- You might even get an additional tax bill because the people that leave trigger a CGT event for you

But at least your superannuation fund will be able to “report” higher returns.