The Tyro Payments Ltd (ASX: TYR) share price has fallen nearly 3% in late morning trade after the company delivered its FY20 result.

Tyro is a finance and technology business engaged in the provision of merchant credit, debit and EFTPOS services. You might have used its software at a retailer or cafe and not even known it existed.

The company listed on the ASX in December 2019 and is Australia’s fifth-largest merchant acquiring bank by terminal count, with 62,722 terminals in circulation at the end of FY20.

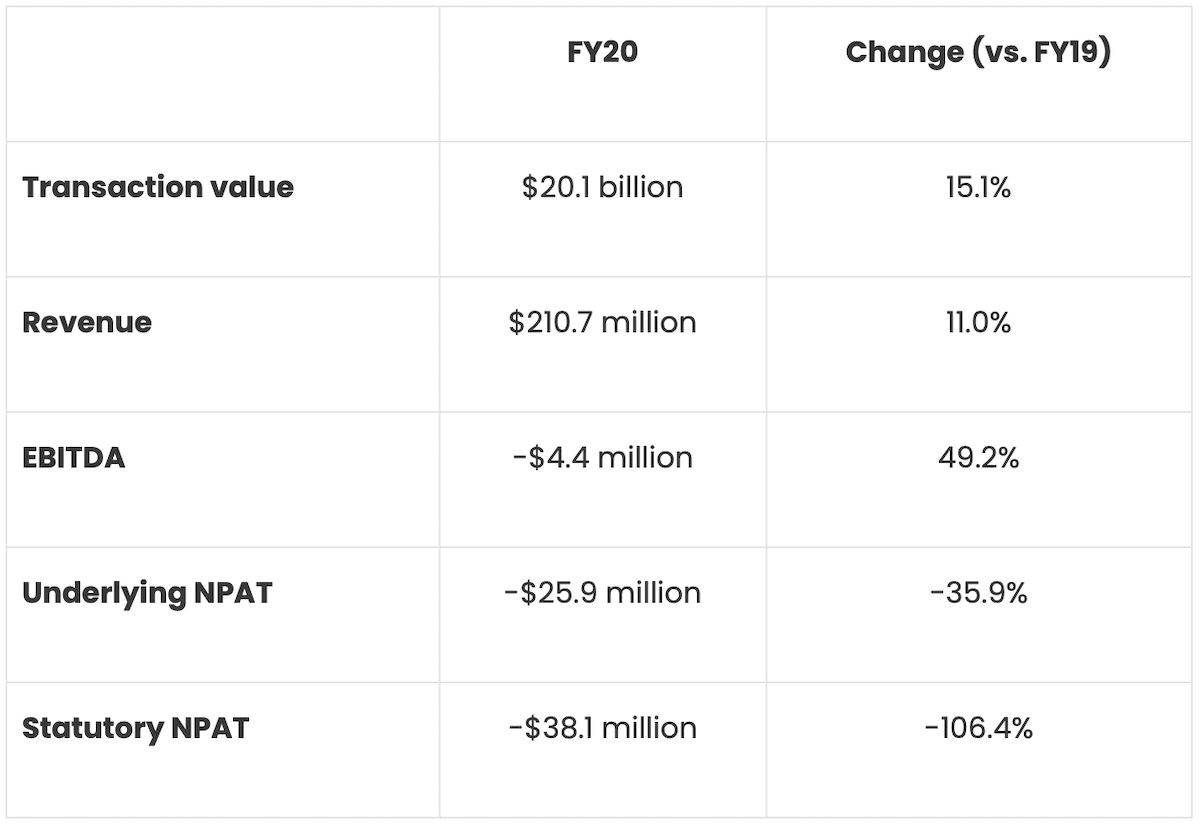

Key points from Tyro’s FY20 report

These transaction value and revenue figures were record results for Tyro, while the underlying net profit after tax (NPAT) result excludes the costs associated with its IPO at the end of last year.

In February, Tyro had been on track to deliver its prospectus forecast, however, the impact of COVID-19 resulted in the company withdrawing its guidance in March.

The majority of Tyro’s 32,176 merchants operate in the hospitality and retail verticals, which have been some of the industries hardest hit by lockdown restrictions. The company noted that transaction value in the hospitality vertical, which was growing at 47% prior to COVID-19, decreased 32% from March to June.

Breaking down revenue, payments contributed $202.8 million, recording 10.4% growth compared to the prior year.

Tyro also has a banking division which offers bank accounts and business loans to small and medium-sized enterprises (SMEs). During FY20, the company grew its number of active bank accounts by more than 50% to 3,600 and achieved a record $60.1 million in loan originations. This led to lending and investment income of $3.6 million, up 31.7% on the prior year.

Additionally, Tyro received $3.9 million from the government’s JobKeeper scheme, which is included in the company’s financial results.

Operating metrics

Tyro’s merchant service fee (MSF) as a percentage of transaction value declined from 0.9269% in FY19 to 0.8953%. While this may appear inconsequential on the surface, remember that Tyro is predominantly a volume-based business that clips the ticket on the payments it processes through its terminals.

Tyro said its lower MSF reflected the onboarding of larger merchants, which are priced on an incremental profit basis, an increase in lower MSF debit card usage, and a reduction in expensive MSF international credit card usage due to COVID-19.

Tyro’s operating leverage was also on show during FY20 as the company narrowed its EBITDA loss by nearly 50% despite revenue increasing just 11%.

Cash flow & balance sheet

At the end of the financial year, Tyro had $122.2 million of cash on its books and no debt.

Turning to the cash flow statement, the company achieved a net operating outflow before banking of $15.7 million. Tyro said this was principally driven by cash spend of $16 million related to IPO costs and terminal purchases of $7.2 million.

Banking balances increased by $23.9 million, reflecting growth in deposits, leading to overall operating cash flows of $8.2 million.

What happens next?

Looking forward, the company said COVID-19 continues to be a challenge, with the second wave of the virus impacting Victorian merchants and the broader consumer sentiment across Australia. Tyro noted that Victoria represents 23% of its transaction value.

Commenting on outlook, CEO and managing director Robbie Cooke said: “Whilst we are not immune to the pressures facing the Australia economy, we have a resilient business model and a determination to continue on our journey of building an ecosystem centred around payments, enhanced by value-adding features and products designed to attract new merchants and retain existing merchants.”

“We remain as convinced as ever as to the opportunity in front of us as we remain focused on our purpose of setting businesses free to get on with business by simplifying payments and banking.”