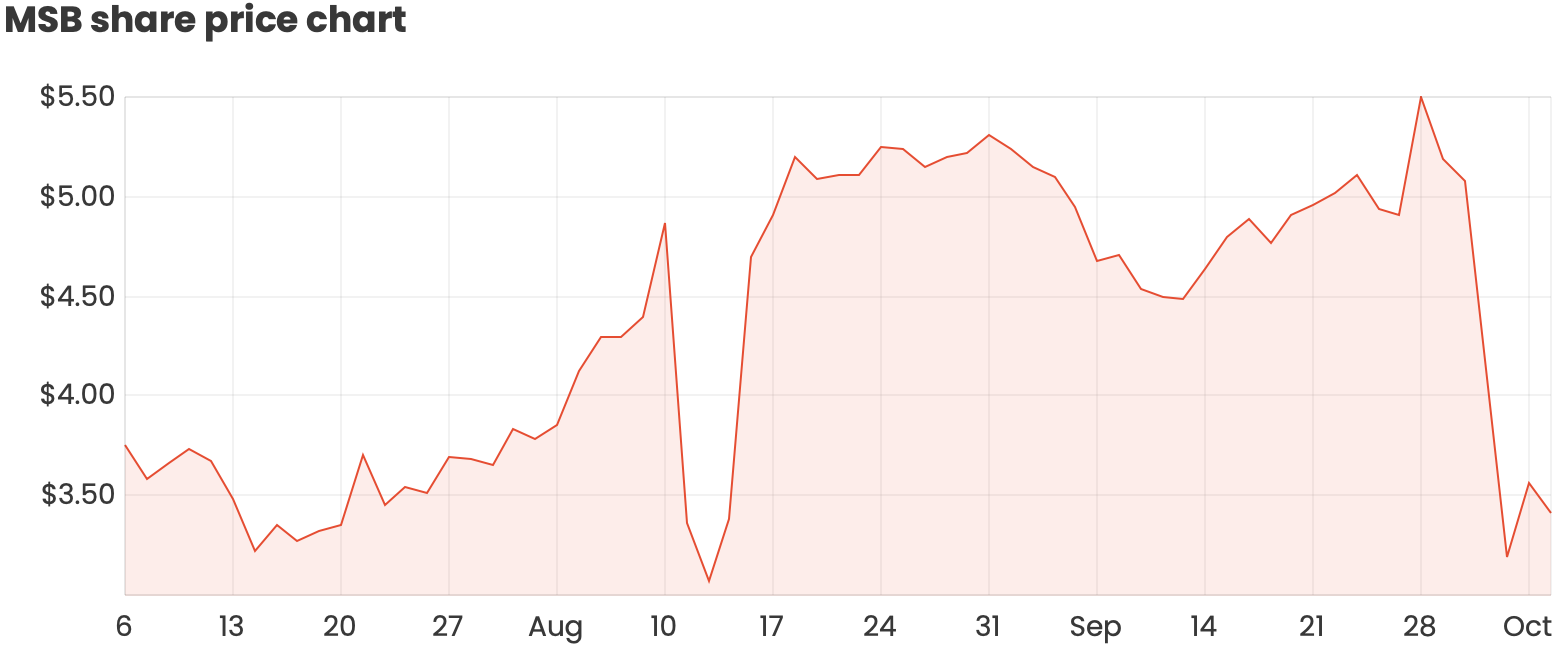

It has been an absolute rollercoaster ride for anyone who has held shares in Mesoblast Limited (ASX: MSB) this year. Multiple announcements, both positive and negative, have seen the Mesoblast share price go in crazy directions in such short time frames.

The last time the Mesoblast share price took a huge dive in August, it subsequently rebounded to even higher levels on the back of a positive announcement.

Given past movements, is it likely we will see a similar recovery? And does this represent a good buying opportunity?

What’s happened to Mesoblast this year?

In case you haven’t been following, last week, Mesoblast shares took a 38% dive following the announcement that the FDA recommended Mesoblast conduct “at least” one additional randomised, controlled study in adults and/or children to provide further evidence to support the effectiveness of remestemcel-L in patients.

Mesoblast will now have a meeting with the FDA, expected within 30 days, to discuss a potential accelerated approval with a post-approval condition for an additional study. Mesoblast can also request an opportunity for a hearing, meaning the response letter can be disputed with the goal of the FDA overturning their previous decision.

The FDA has previously overturned rejected decisions based on safety reasons, so I don’t think it’s out of the question that the FDA could reverse their decision for Mesoblast. The response letter outlined potency concerns of remestemcel-L and asked to provide a further scientific rationale.

Given that the advisory committee voted nine to one in favour of the treatment, approval seems probable, but there’s no certainty in this outcome.

My thoughts on Mesoblast shares

I’m happy to say that Mesoblast is in the too-hard basket at this point in time. I have no background in FDA regulation and approval requirements. Without this edge, I can’t put accurate probabilities on possible outcomes.

To me, this is a punt at best. If you’re happy to take the chance, buying this dip could work out favourably, but there is always the chance the outcome of the upcoming meeting will be perceived negatively by the market.

I don’t like investing in stocks that are contingent on a regulatory approval such as this. A lot of the time the upside is mostly priced into the current share price, meaning you have a lot more to lose, despite it looking like 1-to-1 odds.

I prefer companies that already have solid, predictable cash flows with a clear strategy to drive further growth. I recently wrote an article on Altium Limited (ASX: ALU) which explains why I’ve added it to my buy list.

Altium has launched new products, new costing systems, and unveiled plans to launch into new overseas markets. COVID-19 has affected its operations recently, but I think Altium shares could be a real wealth winner in the long-term.