Out of ideas for ASX growth shares? Here are three shares I’m watching closely at the moment.

Altium

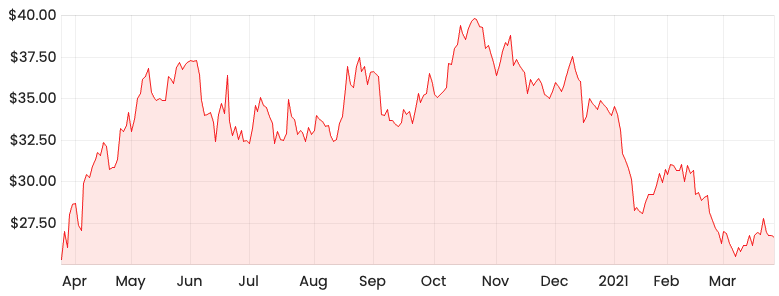

Altium Limited (ASX: ALU) makes software used for the design of printed circuit boards (PCB). After trading around $40 per share late last year, today’s valuation is starting to look a lot more attractive here around $26-$27.

ALU share price

COVID-19 has caused a slowdown in performance, which was highlighted in its HY21 results.

At this stage, it doesn’t seem as though it’s more of a structural change that could cause some ongoing issues, so I’m happy to look past it for now. Another reason why Altium’s valuation has trended downwards is because of rising bond yields and the effect this has on growth companies.

Again, this isn’t affecting the fundamental characteristics I like about the company too much, so it’s not too much of a concern for me.

To read more about Altium, click here to read: Will tech stocks crash in 2021? Here’s 1 ASX share I’d buy if they did.

Lovisa

Lovisa is a retailer of fast fashion jewellery and accessories with 449 stores across 11 countries worldwide.

The company has a vertically-integrated business model, through which it designs, develops, sources and distributes products under the Lovisa brand name.

While COVID-19 has impacted retailing around the globe, Lovisa’s management team has been busy making acquisitions and buying new discounted store locations. As the world continues to push through its recovery, Lovisa will ideally emerge even stronger than it was before.

For more reading on Lovisa: click here to read: Why I think Lovisa is one of the highest quality ASX shares.

Xero

Xero Limited (ASX: XRO) is another ASX growth share that’s starting to look a lot more attractive at current levels.

Xero recently announced it had acquired an e-invoicing platform called Tickstar, which the market reacted quite positively to.

I like that Xero continues to build out its app ecosystem to offer more business services outside of just accounting software.

As Xero’s suite of products become more useful to its customers, this makes customers become more “sticky”, because they’ll forgo many of the benefits of using Xero’s products.

We often talk about network effects quite often here at Rask. Network effects refer to how the value of something increases as the number of users and products grow.

Xero might be a good example of a company with strong potential network effects. This is because its platform is designed in a way that lets outside developers create third-party apps that are able to be integrated into Xero’s platform, improving it along the way.

As the ecosystem grows in size, it can attract more developers, which improves its platform even more.

To read more about Xero: click here to read: Down 28% in 3 months: Are Xero shares in bargain territory?