With the benchmark ASX 200 index just 3% of its all-time high, you could be forgiven for thinking the market is looking a little frothy.

However, I’ve outlined the case for three ASX 200 shares I think are undervalued and offer potentially market-beating returns.

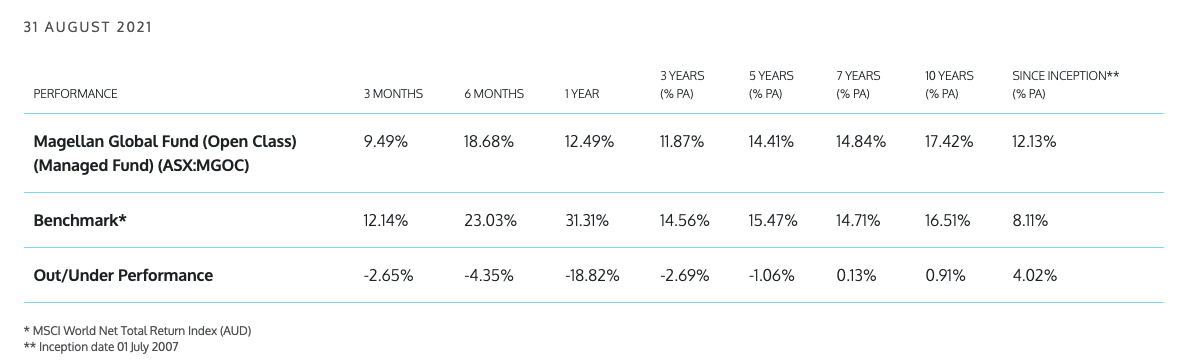

1. Magellan Financial Group Ltd (ASX: MFG)

The Magellan share price is now hovering around prices not since the pandemic hit in March last year. The main reason for the price fall is that the flagship fund has underperformed over the past 12 months affecting overall portfolio performance.

Two things are worth remembering. First, Magellan’s long-term aim is a 9% return per annum after fees, which it has accomplished over every time period.

Secondly, the portfolio is naturally defensive. That means the underlying companies outperform in bad times like during March 2020. Conversely, it aims to maintain or occasionally underperform in bullish periods, as we have seen over the past 18 months.

The key drivers of fees, revenue and profits – funds under management, is still tracking in the right direction.

I think today offers a great buying opportunity for long-term investors or those looking for a 5%+ dividend yield.

2. Tabcorp Holdings Limited (ASX: TAH)

$11 billion Tabcorp is essentially two separate businesses under one name.

It has its wagering division, which provides in-person and online gambling activities. This is a highly competitive, low barrier to entry industry.

Then it has its lottery division, which runs Powerball and Tattslotto jackpots. This is a business with zero direct competition, reliable cash flows and long-dated government licenses.

Tabcorp this year has already received a $4 billion bid for its wagering division. This implies a $7 billion valuation of the lotteries business.

Lotteries recorded $516 million in earnings before tax and interest (EBIT explained) in FY21. This values the monopoly asset at just 12x EBIT.

With the lottery division set to be demerged next year, this should be the catalyst to realise its true value, which I believe could exceed 20x EBIT.

Since most institutions, ETFs and superfunds are restricted from buying Tabcorp because of its gambling activities, I think this is a great chance to buy a share in a monopoly asset before its true value is recognised by the market.

3. Deterra Royalties Ltd (ASX: DRR)

Mining businesses are not usually my cup of tea, however, Deterra is the exception.

In my opinion, this is the simplest business on the ASX.

Essentially it owns a royalty of Mining Area C (MAC) in the Pilbara. Any iron ore sold out of MAC, Deterra receives 1.232%.

This may sound like a small amount, but when you’re digging up millions of tonnes, the numbers start to stack up.

The business has largely zero costs and pays out all of its profits as dividends.

With production set to ramp up 2.4x by 2023, I see this is as a low-risk way to gain exposure to the mining sector.