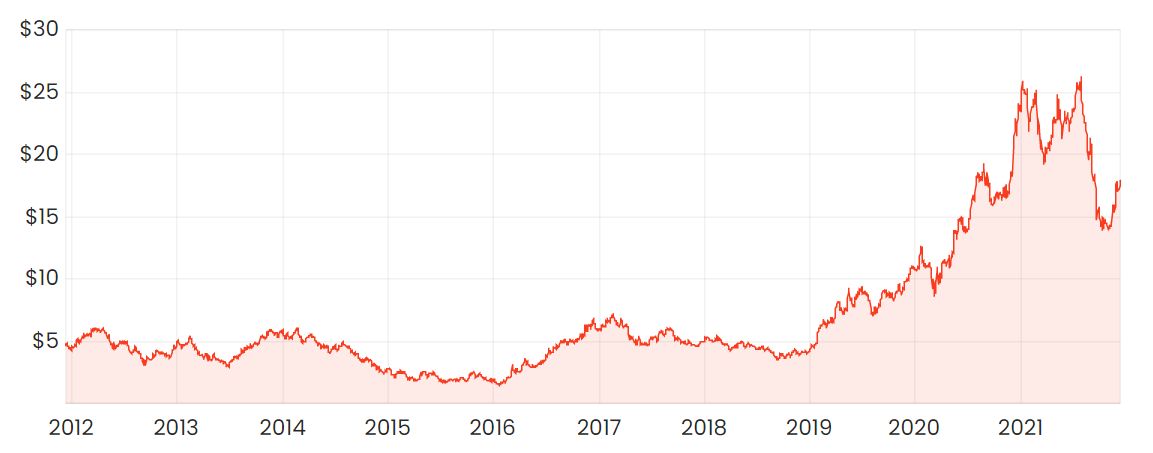

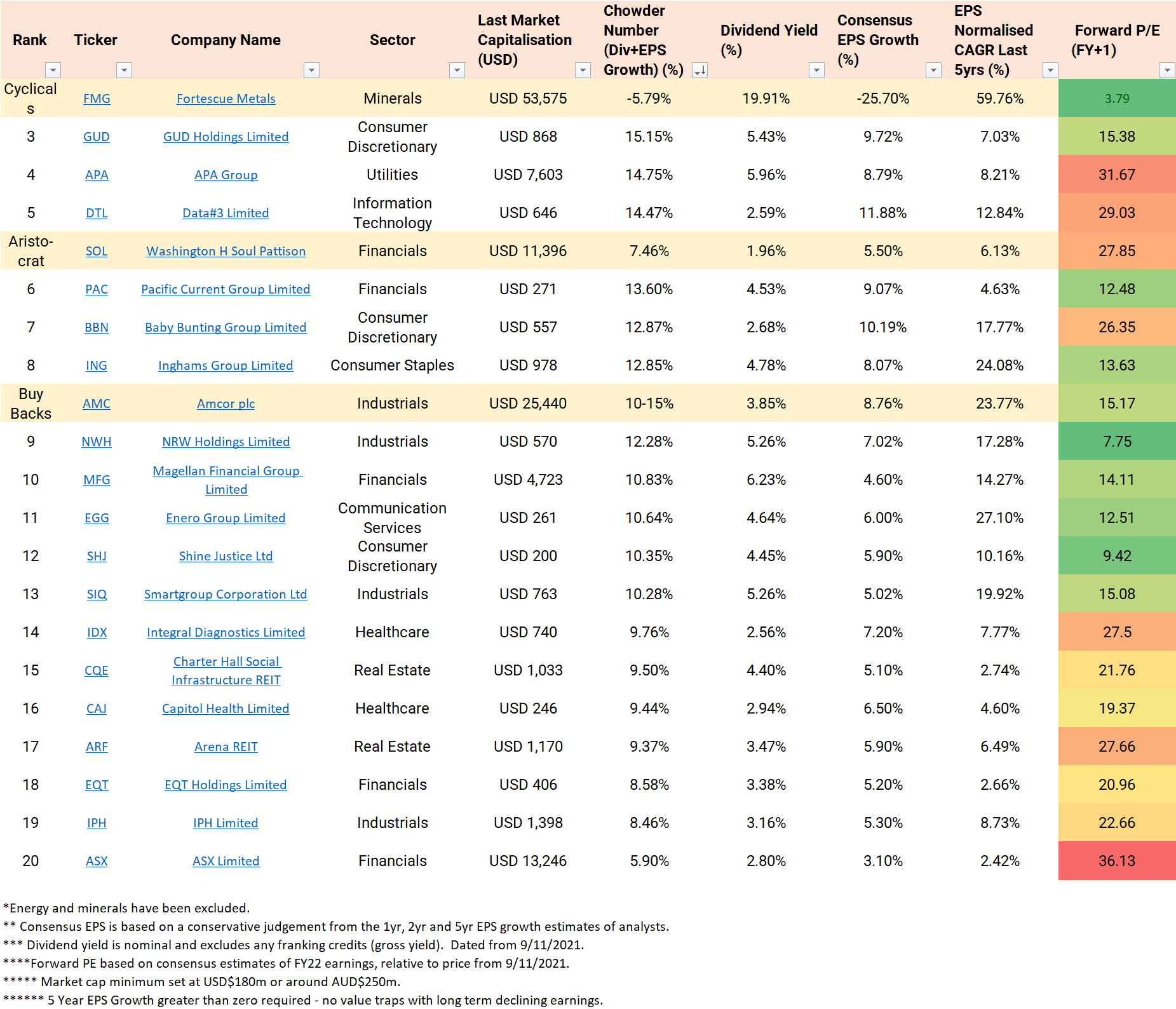

Fortescue Metals Group Ltd (ASX:FMG) has reaped huge returns on the spiking iron ore price. Its dividend yield is a whopping 19.91%, though analysts are predicting an earnings decline of at least -25.70%. Despite the high yield, Fortescue has a negative -5.79% Chowder Number.

Let’s use Fortescue as a case study to explain why cyclicals and dividend growth investing don’t necessarily mix.

FMG share price

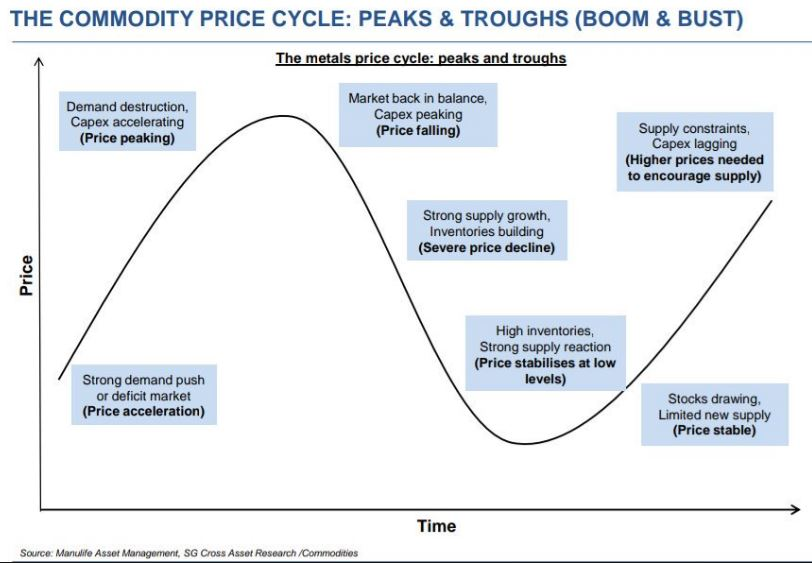

Cyclicals of the ASX

Mining and financials make up around half of the ASX200. Companies within these sectors tend to have boom-bust periods, with returns generally tracking an underlying commodity price. Even a diversified miner like BHP (ASX: BHP) has around ~70% of its revenue from iron ore. And financials such as the Commonwealth Bank of Australia (ASX: CBA) make money from borrowing and lending, which has an underlying commodity price reflected by the interest rates.

The reason for excluding these sectors from dividend growth investing list is not because they can’t pay excellent dividends. On the contrary, through a whole cycle, they are likely to pay more in dividends than industrials, healthcare, or other sectors. Though one requires a different framework for analysis that considers the booms and busts.

What does Fortescue Metals do?

Fortescue is a global leader in the iron ore industry, known for its leading development of world-class infrastructure and mining assets in the Pilbara region of Western Australia. Fortescue was founded in 2003 by Andrew Forrest, who is now one of Australia’s wealthiest people. The vast majority of Fortescue’s iron ore, a steel-making ingredient, is shipped and sold to Chinese customers.

Jaz has written extensively about Fortescue and Fortescue Future Industries. This is their plan to invest in renewable energy and green products, particularly green hydrogen. While future profits may come from there, for now, it’s essentially a pure-play on iron ore.

Is Twiggy Australia’s greatest cyclical investor?

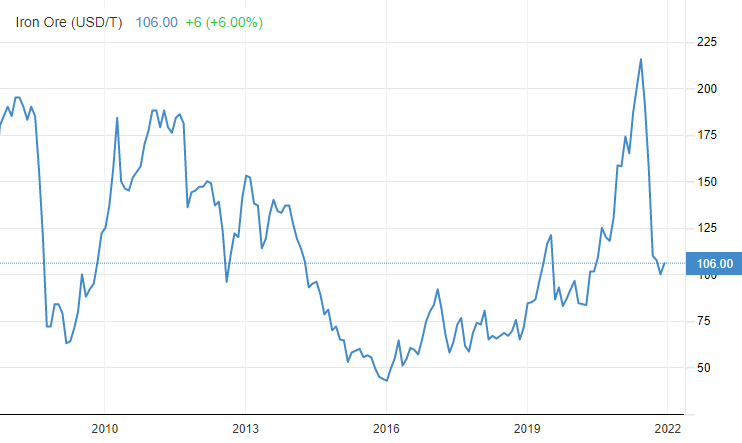

Andrew ‘Twiggy’ Forrest has mastered the art of ‘buying the dips’. Twiggy was buying shares in Fortescue for ~$2 in early 2016 after the iron ore price collapsed to ~$20USD per tonne. Since then, Fortescue has paid over $7.28 in fully franked dividends. In 2020 when Covid hit, he bought another $220m worth at ~$10 per share.

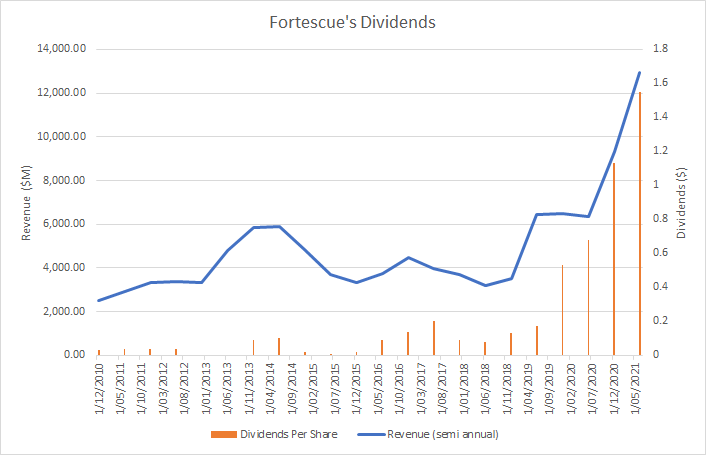

Fortescue’s dividends

Fortescue is currently paying a massive dividend yield of almost 20%. However, looking back through history, this has not always been the case. The dividend has grown, and fallen, with revenues. And since mid-2021, the iron ore price has also halved.

Looking to forward returns

The iron ore price has been depressed but remains above the long-term average and Fortescue’s cost of production. Analysts are expecting at least a 25% drop in earnings, and potentially as bad as 44%. Despite this, Fortescue will no doubt still make a significant profit at US$100 per tonne.

Final thoughts

Dividend growth investing tends to focus more on predictable dividends that increase over time. And indeed, this is where the Chowder Number works best. Finding value in cyclical businesses tends to require an understanding of commodity prices, inventories, industry capital expenditure, and counter-cyclical thinking. For this reason, I have excluded companies like Fortescue from the dividend growth investing list, but not from my investing universe.

For more on Dividend Growth Investing, see my recent article that outlines the screener approach being used here.