DuPont analysis is a method used to evaluate the profitability of an enterprise and the level of return on shareholders’ equity. It uses the relationship between several main financial ratios to comprehensively analyse the financial situation of enterprises. This analysis method was first used by DuPont Company in the United States, so it is called DuPont analysis.

To put it simply, DuPont analysis breaks apart the famous return on equity (ROE) analysis and analyses the operating problems of the target enterprise in a more three-dimensional way. For example, employee performance appraisal has multiple dimensions, while the DuPont analysis method evaluates company performance in multiple dimensions.

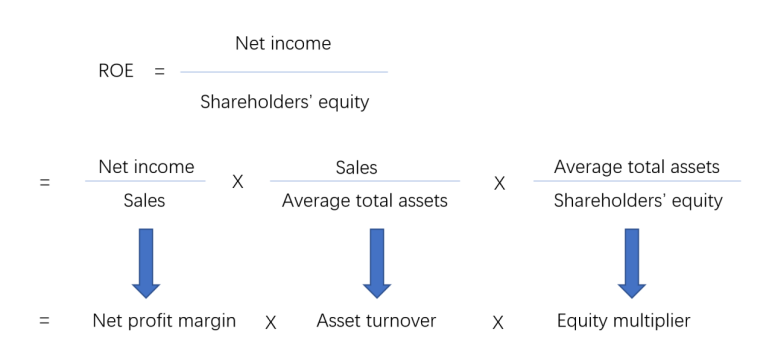

It divides the return on equity (ROE) into three indicators: sales net interest rate, asset turnover and equity multiplier.

- The sales net interest rate represents the profitability of the enterprise, and the formula is the sales net interest rate = net profit/sales revenue; the higher the value, the stronger the profitability.

- The asset turnover ratio represents the operating capacity of an enterprise. The formula is asset turnover ratio = sales revenue/average total assets; the higher the value, the faster the turnover efficiency of the enterprise.

- The equity multiplier represents a firm’s ability to pay its debts. The formula is equity multiplier = average total assets/shareholders’ equity. A higher number means better leverage.

In other words, what the DuPont method tells us is the secret of a successful business, summed up in a nutshell: higher, faster, stronger.

Here’s a quick example:

Suppose Jack and Amy each open a bakery on Washington Street. After some time, Jack calculated the ROE of the two stores and found that he was 25% and Amy’s was 50%.

To understand what went wrong in his store, Jack adopted the DuPont analysis method and reanalysed it.

Jack: 25% (ROE) =20% (net sales rate) * 6.25 (asset turnover) *20% (equity multiplier)

Amy : 50% (ROE) =40%(net interest rate on sales) * 2.5 (asset turnover) *50% (equity multiplier)

By comparison, Jack’s net profit rate is lower than Amy’s . After investigation, it is found that the selling price of Jack’s baguette is the same as Amy’s , but Amy’s cost is much lower than Jack’s, because Amy’s boyfriend is a flour supplier, so the purchase cost is lower.

In terms of asset turnover, Jack’s store has a big advantage, which indicates that its products have performed well in operation.

In terms of equity, Amy’s store is higher. After inquiring, it was found that in addition to opening the shop by herself, Amy also borrowed a lot of money from her friends, so her overall operating capital of Amy was much more than that of Jack.

However, Jack finally gave up the idea of borrowing money from his friends. Higher financial leverage means higher risk, and he didn’t seem to have such a high-risk tolerance.

Knowing the reason for the gap between Jack and his competitors, Jack could find suppliers with lower prices to improve his sales profit margin and borrow some money to increase the equity multiplier of his store.

There are two things you should note; From the perspective of enterprise performance evaluation, the DuPont analysis method only includes financial information, which can not fully reflect the strength of the enterprise and has certain limitations. Therefore, two points should be noted in use:

- In the market competition, the intangible knowledge assets of enterprises are very important to improve the long-term competitiveness of enterprises, but the DuPont analysis method can not solve the valuation problem of intangible assets;

- Financial indicators reflect past performance, but in the era of information technology, customers, supply chains, technological innovation, and other factors have an increasing impact on business performance, and the DuPont analysis method cannot include these aspects.