What’s going on with the S&P 500 (INDEXSP: .INX) share price and the S&P/ASX 200 (INDEXASX: XJO) share price and market rates? David Bassanese of Betashares reveals the current market trends of both the global and the Australian share markets.

Global markets

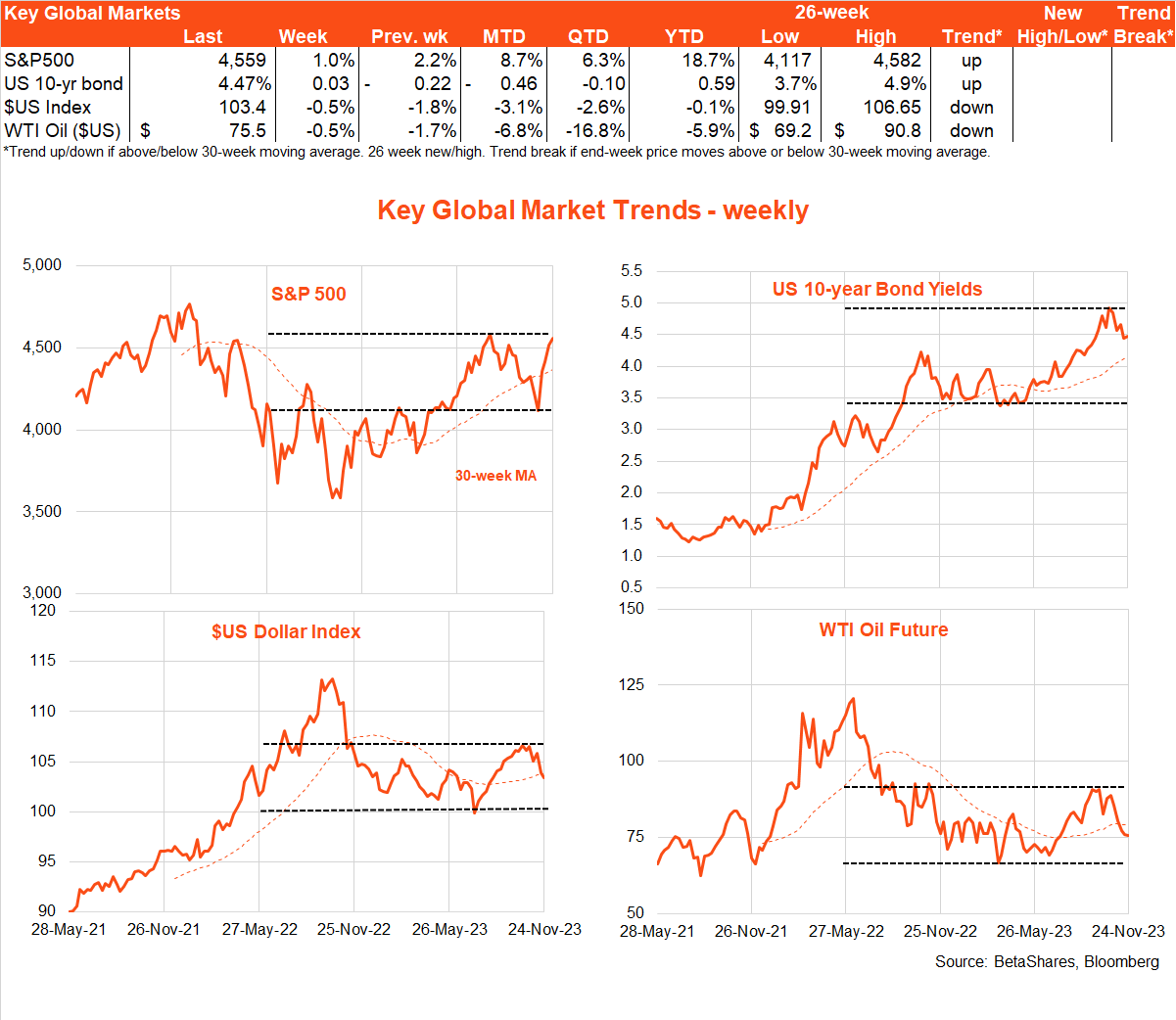

Global equities continued to grind higher last week as the main event – the Fed minutes – did little to dissuade markets from the view that the Fed has finished raising interest rates.

With inflation continuing to ease and some signs of softening in economic growth, the Fed appears to be comfortably on hold with a lingering modest tightening bias.

Bond yields edged back up a touch last week, while the $US continued to weaken.

Also helping sentiment last week was apparent disagreement among OPEC members over whether oil production should be cut deeper to support prices.

The global week ahead will be dominated by the US October private consumption deflator on Thursday (US time).

Hopes are high that the Fed’s preferred measure of consumer price inflation will be as benign as the recently released October CPI report, with headline and core PCE prices expected to rise by 0.1% and 0.2%, respectively.

That would be consistent with a further easing in annual headline PCE from 3.4% to 3.1% and from 3.7% to 3.5% for core annual PCE inflation.

The good news is that the US disinflationary process has started to broaden from the goods to the housing sector, with only core-services (ex housing) showing more feisty resistance.

But with wage growth easing, and potentially consumer spending to a degree, more signs of service-sector disinflation may well emerge in coming months (and potentially this week) which would add to current market optimism that the next Fed move will be to cut rates.

Against this backdrop, also of interest this week will be Thursday’s belated OPEC meeting – which was delayed due to lingering disagreement on production quotas.

It appears Saudi Arabia would like to at least maintain current production levels – if not cut them further – while a few African members are agitating to boost much needed revenues by lifting production.

Last but not least, China releases key manufacturing and service PMI sector surveys on Thursday.

These are expected to show only glacial improvement, with overall conditions in both sectors still relatively muted.

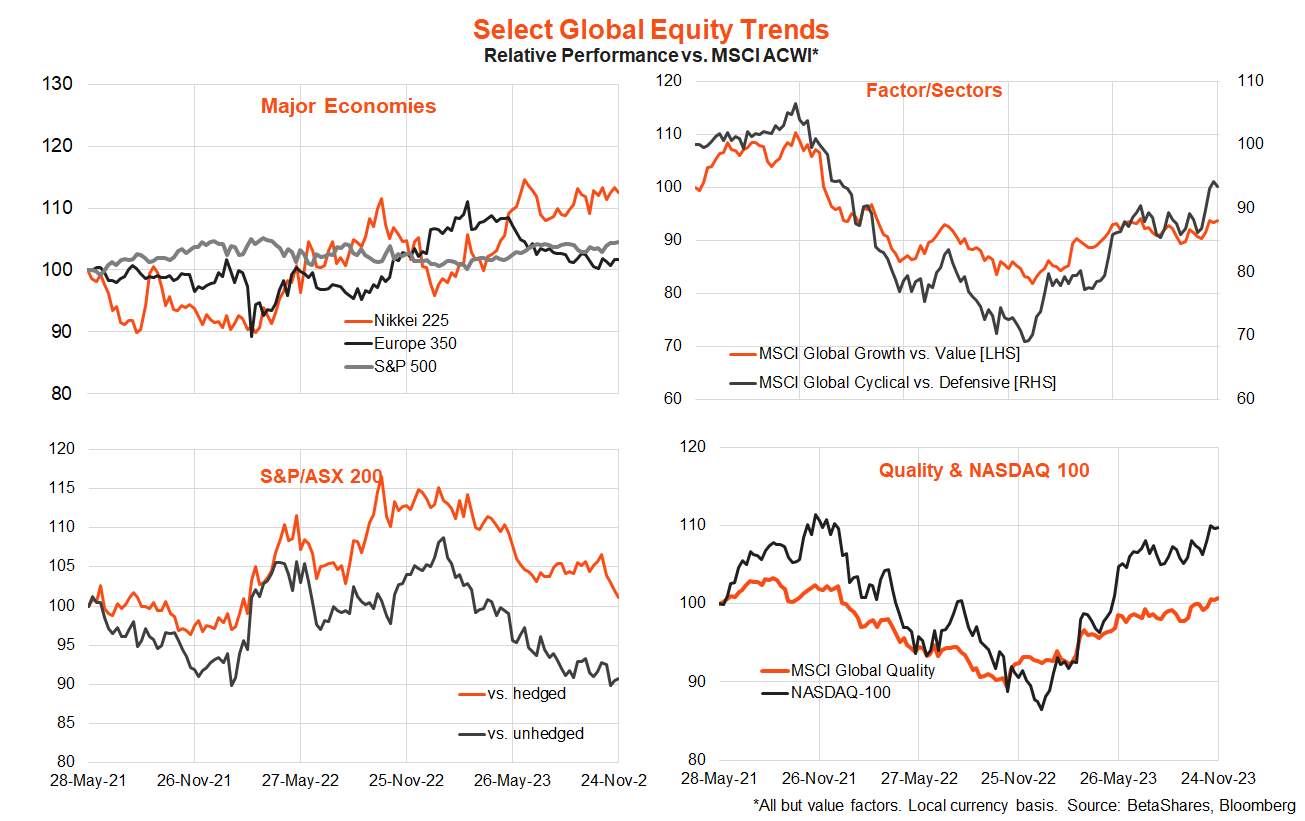

In terms of global equity trends, global quality, the tech-heavy Nasdaq-100 (INDEXNASDAQ: NDX) and cyclicals have perhaps not surprisingly displayed an outperforming bias with the improvement in market optimism in recent weeks.

There is as yet little convincing evidence of a ‘value catch-up’ – not helped by the fact that easing oil prices and bond yields tend not to favour the value-centric energy or financial sectors.

Also of interest is whether Japan can continue to outperform even if the Yen starts to strengthen against the $US.

Australian markets

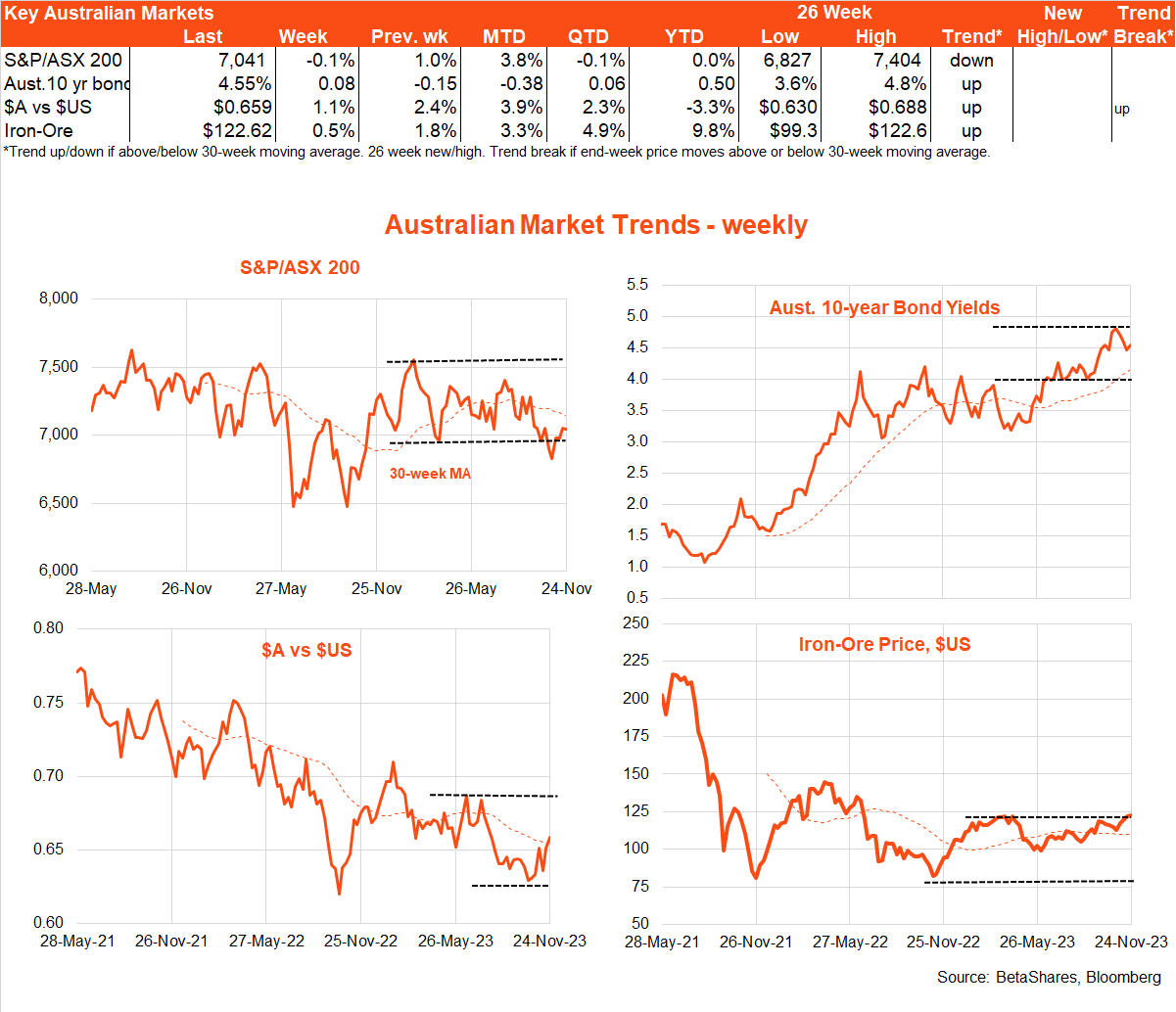

There was little major data in Australia last week, with the main local focus being continued hawkish commentary from the RBA under newly installed Governor Michele Bullock.

Local stocks moved sideways, while the $A strengthened – helped by still-firm iron-ore prices, which are now at the top of their 6-month range.

Despite an apparent sluggish Chinese economy and ailing property sector, its demand for our iron-ore remains firm – due to strength in car production and infrastructure investment.

The minutes to the RBA’s November policy meeting – at which rates were hiked – pointed to a concern that solid demand is allowing business to easily pass on cost increases, and a degree of inflation acquiescence could be creeping into the community.

Adding to the RBA jawboning, Governor Bullock in a key speech pointed to inflation being increasing “home grown” and “demand driven” – seemingly in direct defiance of Federal Treasurer Jim Chalmer’s continued attempt to blame international forces.

All this suggests the RBA retains firmer pressure on the interest rate trigger than the US Federal Reserve at present, and could still hike rates as early as next week if October retail sales tomorrow and the October CPI report on Wednesday are both higher than expected.

Retail sales are expected to lift 0.2% after a feisty 0.9% gain in September (which appeared to partly reflect a delayed Matilda effect and the release of the new iPhone). Annual monthly CPI inflation is expected to ease back to 5.2% from 5.6%, helped by lower petrol prices and a further easing in goods inflation.

That said, due to the staggered incorporation of different pieces of price information on a month-to-month basis, the monthly CPI can tend to be volatile – and there are a number of way to slice and dice the report (along with the headline measure, there is a seasonally adjusted estimate, the annual trimmed mean, and the CPI excluding volatile items and holiday travel).

Given all this potential noise, even if this week’s monthly CPI report surprises on the high side, the RBA might still feel inclined to hold off any decision to raise rates again until February – following release of the Q3 quarterly CPI in late January.

Either way, the market’s implied probability of a less than 5% chance of a rate hike next week seems a little skinny. Given the risk of firm retail sales and inflation reports this week, it is possibly as high as 30% to 40% as of this morning.

Have a greet week!