Visa Inc (NYSE: V) is the most dominant payment network on earth.

Think of Visa’s digital card infrastructure like the autobahn for payments.

In 2023 alone, over 276 billion transactions were processed on Visa, meaning a staggering U$12.3 trillion was sent across 160 different currencies and over 200 countries and territories. That’s a whole lotta mulla arriving safely and securely, all without skipping a beat.

Its payments infrastructure (known as VisaNet) lies at the centre of digital transactions and sits in the sweet spot for all transactions, creating a powerful business model that functions like the internet’s toll booth. Taking a tiny little cut of the 76,000 transactions that it makes happen every second.

Here are three major reasons I fell in love with Visa, and still love it today.

1. Network effects

Visa created one of the strongest network effects I have ever seen.

With an ever-growing army of cardholders and merchants busy like worker ants building out its payment tunnels, growth has come easy for Visa’s economic moat.

In FY2023, Visa’s number of merchant locations increased by 17%, bringing the total to over 130 million places that accept 4.3 billion Visa-branded credit and debit cards. That’s strong growth for a payments company that has been there from the start.

The more cardholders there are, the more stores accept Visa. The more stores that take Visa, the more people will want Visa cards.

This flywheel has scaled Visa’s network to smash even the most bullish expectations, with its total market size and penetration being underestimated time and time again.

2. High margin, capital-light

Adding to an already great recipe is Visa’s market-leading margins and capital-light business model.

Since Visa’s network isn’t physical, its costs remain relatively fixed. The incremental costs of running more transactions over its network plummet against a revenue base that has scaled impressively.

By essentially monopolising network routing, authentication and card licensing, Visa and its shareholders have positioned themselves in the very sweet spot of payments.

With juicy 52% net profit margins, pound for pound this makes Visa is one of the most profitable businesses on Earth.

For shareholders, it means Visa is churning bucketloads of free cash flow every day.

3. Transition to digital payments

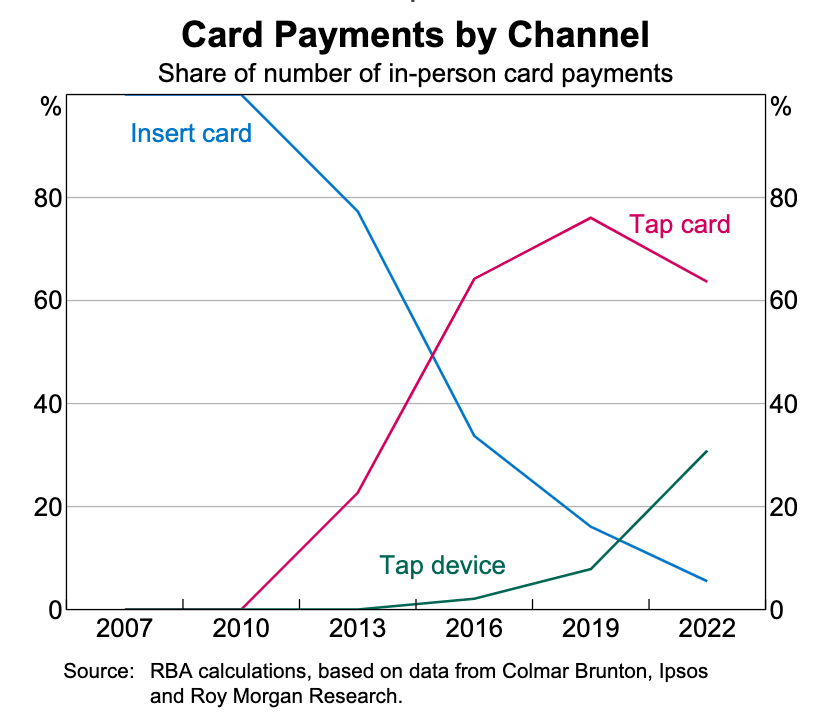

While the phrase goes “cash is King”, in reality, the meteoric rise of digital payments has all but displaced cash in Australia.

RBA data shows card payments have quickly become the payment method for Aussies and it’s easy to see why. Nearly 80% of payments are electronic.

Paying with plastic means faster and secure transactions for everyone. People now don’t need to fumble and count notes or coins, and trips to the ATM are fewer and far in-between.

Driving this rapid adoption curve has been the rise of e-commerce, advancements like contactless payments, and the recent shift to mobile and smartwatch payments through services like Apple and Google Pay.

Not to mention a global pandemic which only added further fuel to the fire, forcing tap-to-pay and mobile wallets mainstream. By removing what little friction there was left, Visa has found yet another growth accelerator to make payments run faster and even more secure.

Bottom line

Visa ticks a lot of boxes.

Not only is it one of those great businesses that continues to surprise investors over the long term, but it has one of the strongest moats I have ever researched.

With a dominant market position and a business model that sits in the sweet spot of the fintech ecosystem, Visa’s margins translate directly into juicy cash flows.

Add in the momentum of digital payments displacing cash, and I’m backing Visa to keep doing its thing in the background, unlocking huge value and making sure money gets to exactly where it needs to go.

Disclosure: Kevin owns shares in Visa (NYSE: V)